Stormy Weather on the OpenSea

A $13.3B crypto startup lost 90% of its revenue. Can it survive its self-described "crypto winter"?

Of all the wildly avaricious, blatantly illegal, and disgustingly immoral things in crypto, few elicit a stronger response than NFTs.

NFTs are a lot of things, but boring they are not. It’s hard to be on the fence about them. They’re either the future of art and ownership. Or they are scams designed to separate the dumb and the greedy from their money - planet-destroying carbon emissions included.

I, for one, remain cautiously optimistic about NFTs. But that’s a story for another time.

If you wanted to buy NFTs, for the longest time, there was only one marketplace in town: OpenSea.

OpenSea isn’t quite in the business of selling shovels in a gold rush. Rather, it’s the auction house where prospectors hold aloft their shiny rocks and invite bids from speculators.

For a while, it was the only such auction house in town of any worthwhile scale. Business was good. There were more bidders, prospectors, and shiny rocks you could count. A bad month was $100M in volume. A good one topped $400M.

The peak was an eyebrow-raising funding round: $300M at $13.3B valuation.

And yet, it all fell apart - in the spectacular collapse that only crypto can create. Volume has disappeared, floors have cratered, and once-thriving communities now resemble ghost towns.

So what went wrong?

There’s a lot to unpack in OpenSea’s misfortunes. Some of the missteps were forced by the market. Some others can be attributed to a basic misunderstanding of the business itself.

Let’s dig in.

Declining Revenues, Departing Users

First, let’s look at where we are.

1. OpenSea’s volume topped out in January 2022 - the same month it raised its monster Series-C round.

In January 2022, $4.857B worth of NFTs were traded on OpenSea’s Ethereum marketplace. An additional $79.13M worth of NFTs exchanged hands on the OS Polygon marketplace - rounding error compared to the Ethereum volume.

VCs and buying tops - name a better combo.

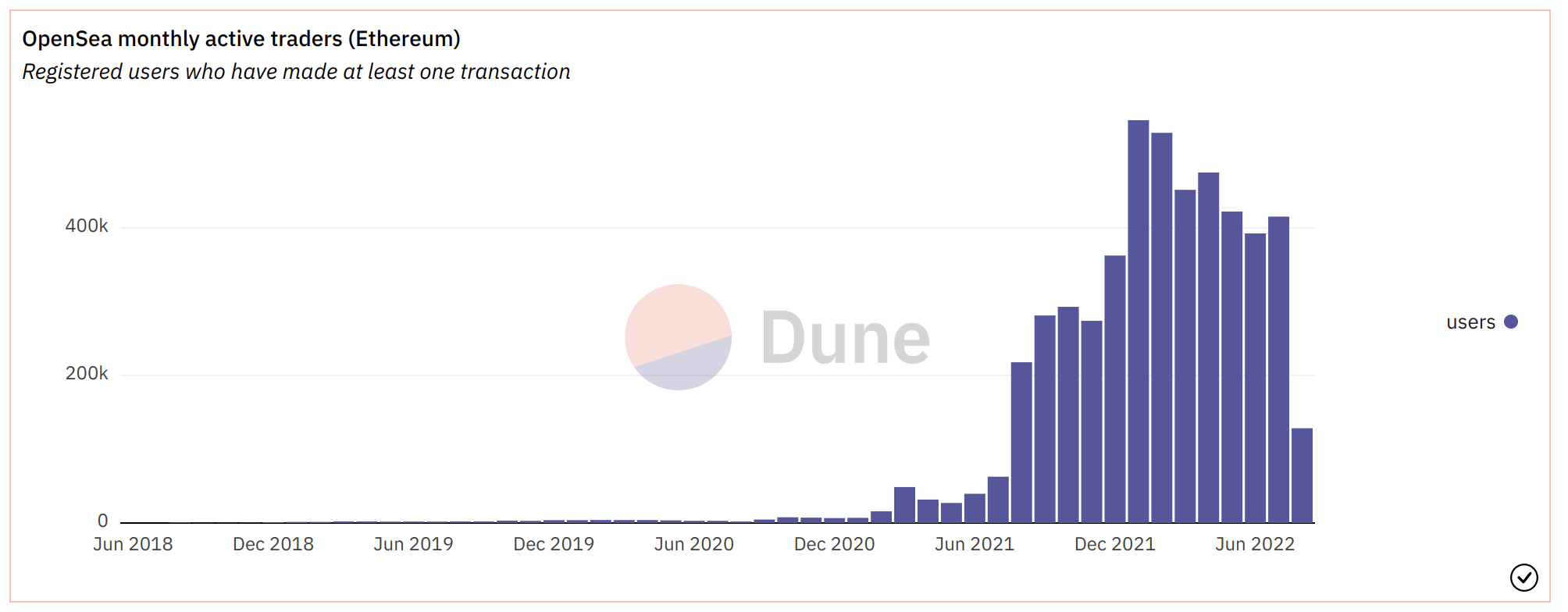

2. Monthly users topped out in January 2022 as well.

January 2022 was the month when NFT mania hit its peak. Celebrities were “buying” them (more on this in another article), including heavyweights like Eminem and Justin Bieber. Of course, celebrities dragged retail into the fold - monthly users jumped over 50% from December ‘21 to January ‘22.

3. Usage - and users - dropped as NFTs and other risk-assets took a beating.

Active monthly traders decreased almost 24% from the January peak to 415k in August. Total trade volume drop was more drastic - from a peak of $4.85B to $528M, a drop of nearly 89%.

Some of this can be attributed to the drop in Ethereum prices. But it’s safe to say that most traders don’t want to hold onto illiquid jpegs while everything is crashing around them.

4. Monthly revenues collapsed as volume disappeared.

OpenSea charges a 2.5% fee on every transaction. This fee is paid in Ethereum. While it's not clear when and how OpenSea converts its Ethereum holdings to fiat, given the massive January volume, OS likely made between $120M to $146M in January 2022 - give or take a few dozen million based on Ethereum prices.

5. The price of every traded NFT has been going down.

The NFT market isn’t immune to the selloff in risk assets. In January, the average price of every NFT that exchanged hands was $2,125. Since then, the total number of NFT trades has been robust while the overall trade volume (in $ terms) has slumped.

In July, the average price of an NFT sold on the marketplace was $310 - a drop of 85%.

If you were a particularly optimistic VC, the $13.3B valuation might have felt cheap in January. After all, this was a business doing $100M+ in monthly revenue.

Moreover, it had the right narratives. Of course, NFTs are the future. Of course, everyone is going to buy NFTs. Of course, they were all going to buy them on OpenSea.

And of course, things didn’t go to plan.

It’s easy to get tunnel vision when your Twitter feed is filled with Snoop Dogg shilling jpeg after jpeg. If Snoop could “get it”, surely others will too - eventually.

3 Challenges to OpenSea’s Dominance

Regardless of whether the NFT market makes a comeback, there’s a good chance OpenSea won’t see its old highs in the near future.

Three reasons:

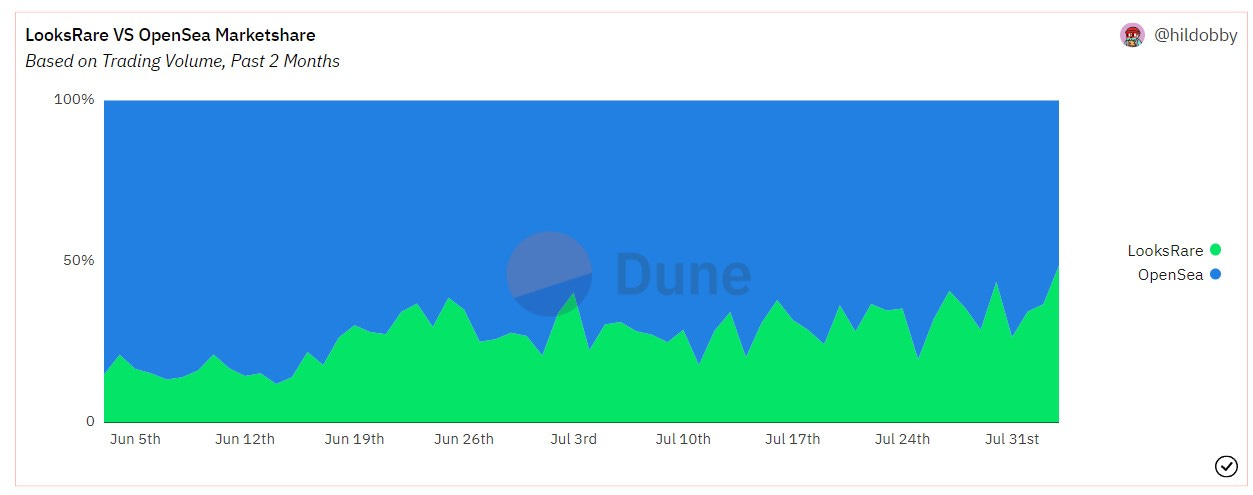

1. Competitors have stolen market share, thanks in part to generous airdrops.

Besides recording the highest-ever trade volume for NFTs, January ‘22 was also the month OpenSea had its first major competitor - LooksRare.

There have been competitors before, but they either missed the “10,000 PFP collection” hype train (Rarible), or they focused on one-off pieces (SuperRare).

LooksRare, however, was a direct competitor and it offered two things OpenSea didn’t:

A generous airdrop

The ability to earn a share of the fees

While data for LooksRare usage is clouded because of wash trading, it's undeinable that the volume has been trending up.

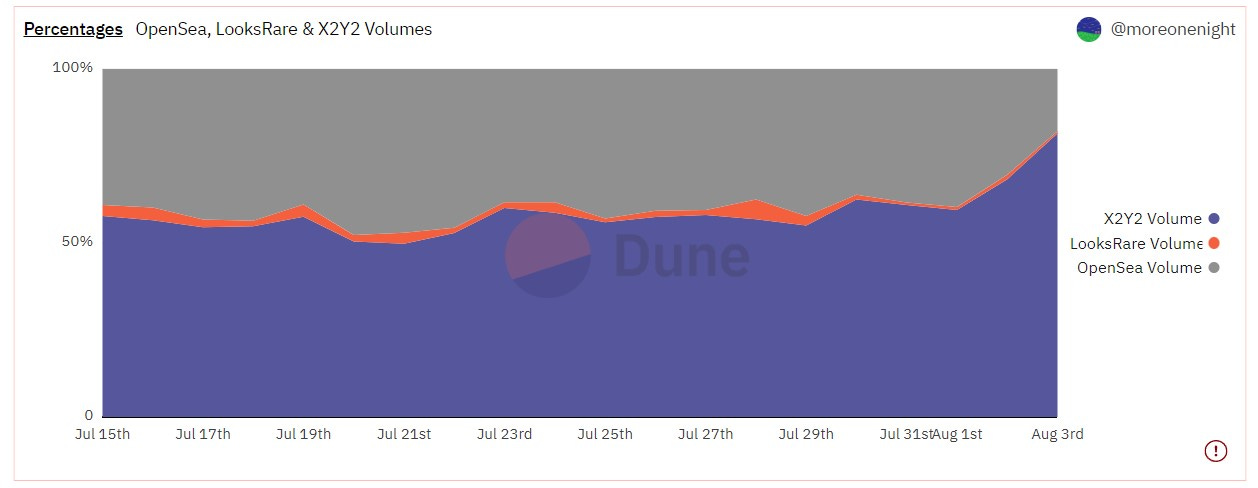

Meanwhile another competitor with a focus on the Asian market, X2Y2, started gaining strength. By July ‘22, its volume had exploded. While wash trading remains a problem, data shows that X2Y2 has already exceeded OpenSea’s volume.

Both of these protocols gave away their users fat airdrops. They also offer them token rewards for trading, while also charging lower fees.

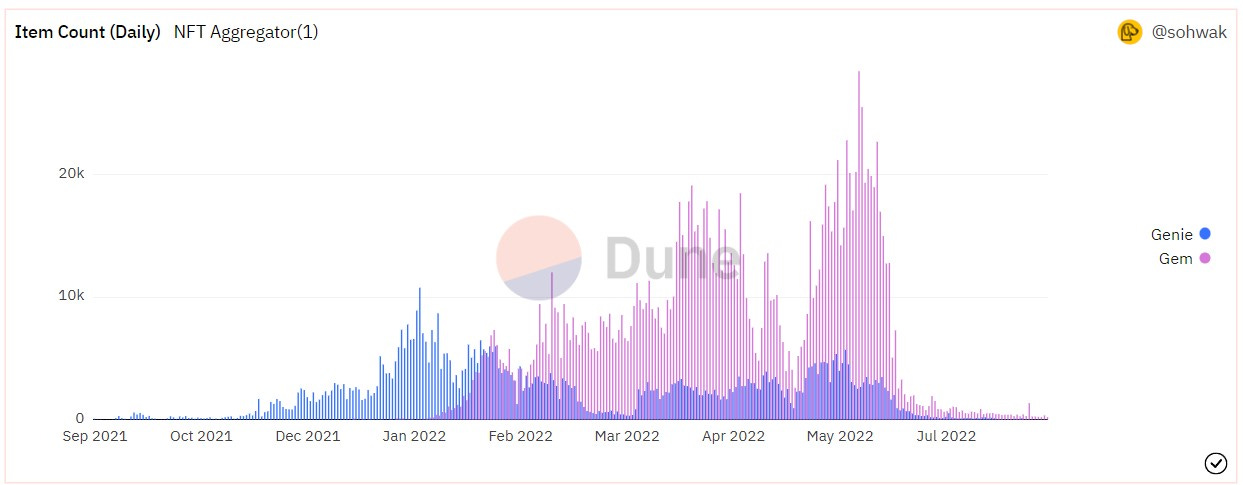

2. Aggregators have made NFT purchases ‘platform agnostic’.

If you were a simple degen who wanted to buy half a dozen NFTs to flip for a profit, you wouldn’t care what platform you buy your NFTs from - you’d just want the cheapest price.

Aggregators such as Gem and Genie were built exactly for this use case - both even have a “sweep” feature to buy NFTs in bulk..

These aggregators have blurred the boundaries between the NFT platforms. Users get access to all the NFTs listed at every platform, even if they don’t have an account there. OpenSea’s competitive advantage - access to a massive user base - was effectively nullified.

To give you an idea of the scale, at their peak volume, Gem and Genie combined had roughly 15% as many NFT sales as all of OpenSea.

I won’t even mention all the minor controversies, from insider trading to exploits to unfavorable press to general NFT/crypto backlash. But the results are clear:

3. There is no inventory edge.

The open nature of blockchains means that there is no such thing as “exclusivity”. If it’s on the blockchain, it can be listed by anyone without prior permission.

This means that a competitor can bootstrap a massive inventory list right at launch. While you do need to bring owners onboard, our new NFT marketplace at least won’t have empty display cases.

Getting owners onboard isn’t particularly tricky either. Since owners want to sell for the highest possible profits, they are destined to accept bids from the platform with the lowest fee. A 10ETH sale is the same, regardless of whether it comes from OpenSea or X2Y2. Just that one charges a 2.5% while the other does it at 0.5%.

The end result is an endless war of attrition where competitors keep undercutting each other’s fees to grab a share of the market. you can launch a new NFT marketplace and be assured that at least your display cases won’t look empty.

Getting owners onboard isn’t particularly tricky either. Since owners want to sell for the highest possible profits, they are destined to accept bids from the platform with the lowest fee.

The end result is an endless war of attrition as competitors keep undercutting OpenSea’s 2.5% fee to get market share.

This brings us to the big question: what did OpenSea do wrong?

While the market drawdown hasn’t helped, I believe OpenSea also fundamentally misunderstood the NFT marketplace and its own role in it.

The NFT Market Has Changed

On paper, NFTs are, well, non-fungible. Unlike Bitcoin where every coin is just like another, every NFT is unique. Bored Ape #5162 is unlike Bored Ape #9610.

It stands to reason that collectors will prefer buying rare or better looking NFTs, often paying a premium.

That’s the theory.

In reality, collectors have been edged out of the market by traders. To a trader, NFTs are largely fungible. One floor jpeg is just like another; buy the cheapest of the floor so you can flip for a profit.

Sure, rare traits are good to have, but if the goal is to sell to another equally rarity-blind trader, the only thing that matters is price.

In this trader-led market, the goal of NFT platforms shifts as well. You’re no longer in the business of discovery; you’re in the business of facilitating rapid exchange of fungible goods.

Think more NYSE than Christie’s.

And that’s a problem.

OpenSea isn’t a Platform

OpenSea would like to tell you that it’s a “platform”. Most users will call it a “marketplace”.

In practice, OpenSea has morphed into something entirely different: an exchange.

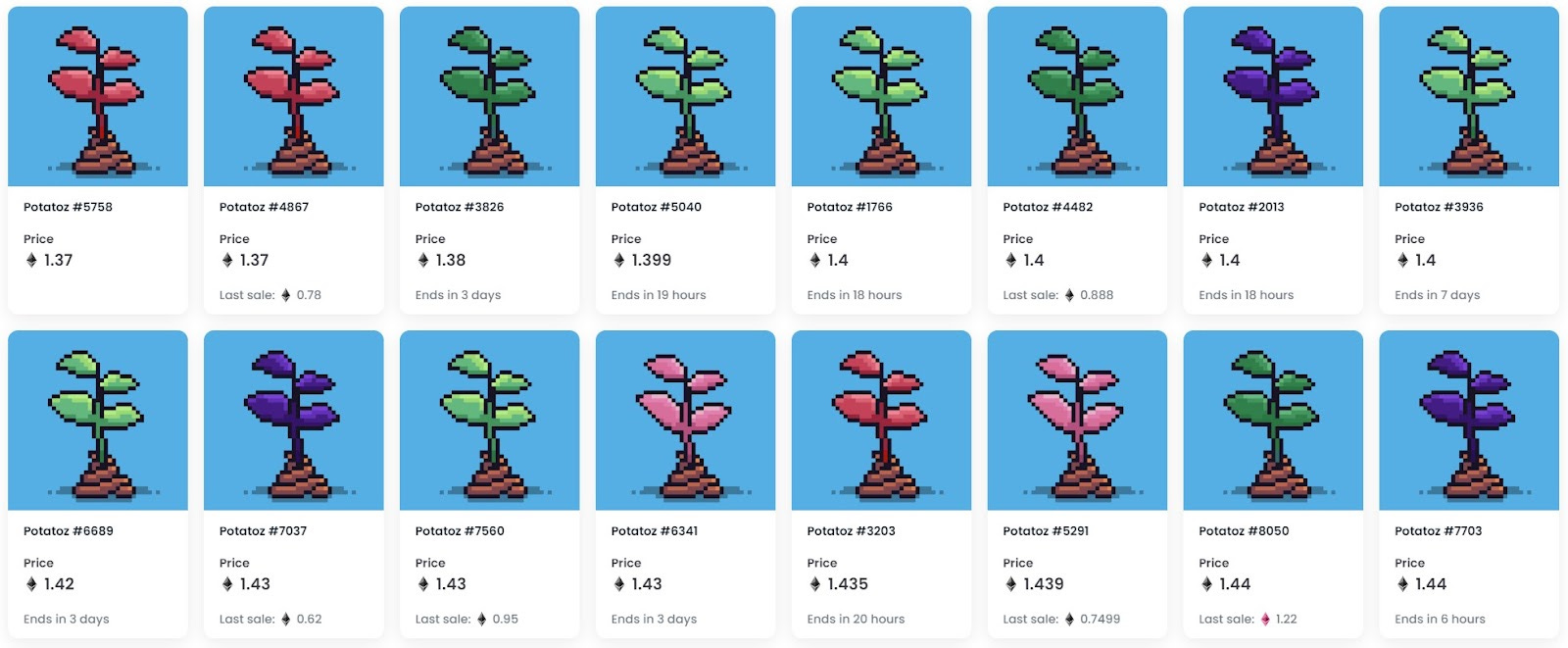

Look at the floor prices for any NFT collection on OpenSea. Sort by low-to-high. Notice the price gap between individual items.

Here’s The Potatoz.

Does the narrow pricing gap between individual items resemble a true marketplace (like Amazon)? Or does it more resemble an exchange order book?

Think of prices off the floor as the Ask in an exchange order book. Collection offers - the lowest price you’re willing to pay for any NFT in the collection - as the order book Bids.

In fact, nothing exemplifies the increasing fungibility of NFTs than the very idea of “Collection Offers”. This shows that market participants simply do not care what NFT they get, as long as they get it at the lowest possible price.

This is OpenSea’s blind spot - the belief that they’re in the business of making rare digital goods available to end users.

The truth is that OpenSea now functions largely like an exchange. Assets are traded not to be held, but to simply be bought and sold for profit.

In a marketplace, fees are not critical to purchase decisions. Individual items exchange hands infrequently enough that a 2.5% fee is an afterthought.

But in an exchange, a 2.5% fee is prohibitively expensive and cuts into profits for each trade.

OpenSea’s competitors seem to understand this. LooksRare charges a 2% fee. X2Y2 charges just 0.5%. SudoSwap is at 0.5% as well.

OpenSea’s current fee model is simply unsustainable. It’s also built for a NFT market that doesn’t exist anymore.

I suspect before the end of this year, we will see some platforms offer fees below 0.25%, which would be fitting for an exchange - but disastrous for OpenSea’s margins.

Ignoring Decentralization (and Degens)

If there’s any original sin in crypto, it’s this: not having a token.

Crypto users want to buy tokens.

Sure, they want to flip NFTs and deposit their dollars to get yield. But more than anything else, they want to buy tokens, talk tokens, chart tokens, and stake tokens.

And a token is exactly what’s missing from OpenSea.

While it's easy to understand why (especially given the regulatory gray areas), the lack of a token creates a gaping hole from which all degens, whales, flippers, and memers can slip through. If competitors can offer tokens with staking and liquidity pooling rewards and fee sharing, OpenSea’s competitive arsenal suddenly looks emptier.

At the heart of this token-deficit is perhaps a core mismatch between the kind of users OpenSea aspires to attract vs what it actually attracts. The NFT market is driven largely by whales trading massive amounts of ETH for jpegs of questionable quality, with retail following closely behind.

In the absence of a token to ape and fee to be shared, whales will simply move to other platforms, especially ones that offer cheaper fees.

Why list your $100k ape on OpenSea (and pay $2,500 in fees) when you can list it on X2Y2 and earn token rewards while only paying $500 in fees?

OpenSea could ignore tokens and charge its 2.5% cut when it was the only game in town.

Now with competition getting tougher and market conditions changing, a course correction is crucial.

If you enjoyed this post, consider subscribing. I write occassional long-form pieces on Web3 and its convergence with Web2, NFTs, tokenization, and the future of crypto.